Our newsletters are intended to keep you up to date on

pertinent industry news and offer more in-depth insight into various

types of coverage and endorsements. We publish our newsletters

at least once each quarter. We hope you enjoy it.

Thank you for your patronage!

What is a "Manifestation

of Willingness to Renew" And Why Does It Matter?

From time to

time, a few of our insurers may issue documents on your

insurance policies that may seem unnecessary to you. We've

had a few questions about these in recent weeks, so we

thought we'd take a moment to address them.

Most insurance

companies begin working on issuing renewal policies or quotes

somewhere between 120 and 60 days prior to the expiration of that

policy. So if your policy expires on January 15th, there's a

good chance your insurer is already examining your policy and

deciding if they want to renew it, at what premium they would be willing

to do so, and whether or not there are any changes to their coverage

they want to implement.

That 60 day mark is

important to companies, because if they want to change the language

of a policy or get off of it completely,

they're obligated by insurance regulations to send a notice

at least 60 days prior to the expiration of that policy (in Illinois

and Missouri, Indiana has different regulations that vary based on

the type of policy in question). The Department of Insurance

for these respective states have set this deadline so that consumers

aren't left scrambling for coverage at the last minute. If an

insurer misses that deadline, they're obligated to renew coverage as

it was the prior year.

If a carrier

is going the non-renewal route, they would issue a "Notice of

Non-Renewal" to the policy holder. If they're changing the

wording of their policies, they have to issue a different type of

notice, typically a "Manifestation of Willingness to Renew"

or a "Notice of Conditional Renewal." Basically,

the latter of these notices say "we

are willing to continue writing this policy for you, but with the

following changes to the policy form." They

will then include an outline of the changes being made.

These

modifications to policy language could happen for a variety of

reasons. Often times, they're simply to

clarify wording. Occasionally, they are to broaden

coverage provided and sometimes they restrict coverage. In

almost all instances, it's because past claims and incidents

have brought existing policy language under closer scrutiny,

hence the company's desire to clarify, expand or restrict the

wording to what was originally intended.

They can be

confusing; usually they'll only reference the section and paragraph

of the change and the change in wording. To get a better idea

of the full extent of the change, you'd have to dust off your

policies and go digging through them to read the complete section or

paragraph to try to understand the change.

If there's ever a

change that would have us concerned about

the comprehensiveness of your protection, we would address

that directly to you and, of course, look for alternatives, if

the situation warranted.

Winter Fire Safety Tips

The single most important thing you can do to keep

your family and business safe from fire is to have a smoke alarm in

every bedroom and on every level of your house. Smoke alarms

reduce the risk of home fire deaths by 50 percent.

With winter approaching, it is important to remember

certain safety rules when heating your home or business.

Furnaces

A malfunctioning furnace can produce carbon monoxide,

a "silent killer," that can spread throughout your house,

and an undetected gas leak can create a highly flammable and explosive

environment.

Change

the unit's filter once a month and have a qualified professional

check the unit once a year. Install carbon monoxide

detectors, following manufacturers guidelines.

Be

sure all furnace controls and emergency shutoffs are in proper

working condition. Leave all furnace repairs to qualified

specialists - DO NOT attempt repairs yourself.

Inspect

the walls and ceiling near the furnace and along the chimney

line. If the wall is hot or discolored, additional pipe

insulation or clearance may be required.

Ensure

the flue pipe and pipe seams are well supported and free of

holes or cracks. Look for soot along or around seams, as

this can indicate a leak.

Check

the chimney to make sure it is solid; are there cracks or loose

bricks? All unused flue openings should be sealed with

solid masonry.

Keep

trash and other combustibles away from the heating system.

Wood burning appliances: stoves

and fireplaces

Most experts do not recommend the installation of any

wood-burning stove unless it is airtight and has controlled airflow

(wood-burning stoves are also a major concern of home insurers).

If you are burning a lot of wood, your stovepipe and chimney

may have a heavy buildup of creosote, which can lead to a fire in

your chimney and spread to the roof of your house.

Fireplace

chimneys should be inspected and cleaned at least once a year,

and stovepipe chimneys should be checked once a month and

cleaned as needed.

Ensure

proper installation. Adequate clearance for wood stoves is

at least 36 inches from combustible surfaces.

Wood

stoves should be of good quality, solid construction and design

and UL listed.

Do

not use lighter fluid, charcoal starter, gasoline or other

flammable liquids to start or accelerate the fire.

Keep

a glass or metal screen in front of the fireplace to prevent

embers or sparks from escaping. The area under and in

front of the unit should be made of noncombustible substance.

No carpets or throw rugs.

Never

burn charcoal indoors! Burning charcoal can give off

lethal amounts of carbon monoxide.

Before

you go to sleep, be sure your fire is out. Never close

your damper with hot ashes in the fireplace or wood stove.

A closed damper can help rekindle the fire, forcing toxic

carbon monoxide into the house.

Never

break a synthetic log apart to quicken the fire, and never use

more than one log at a time. They often burn unevenly,

releasing higher levels of carbon monoxide.

When

emptying the ashes from the wood stove or fireplace, put them in

a metal container and place outside the building. Let them

sit for a while to cool, or add water to the container to make

sure all the ashes are out before disposing of them.

Other

Winter Fire Threats - Holiday Specific

Each year,

there are an estimated 10,000 fires involving Christmas Trees. Most

of these involved short circuits from the use of extension cords or

connecting too many strans of lights. One of our favorite

episodes of Mythbusters

involved tests to see if the heat from Christmas lights could spark a fire

- they did not. And as tests by the National Fire Protection

Association show, when a dry tree goes up in flames, it goes fast.

Another more common

holiday fire involves frying turkeys. The news clip below has

some some safety advice for those using fryers this Thanksgiving.

Spotlight On: Crime Insurance

Don't Get Robbed Twice -

Understand Crime Insurance

First

off, some scenarios:

1. Your

business has been burglarized and you find yourself standing amid

broken glass. There's trashed shelving, broken displays and missing

merchandise. While vowing revenge the thought comes to you mind: will

my insurance cover this?

2. You

realize your favorite cashier is stealing from you. Taking $20 here

and $50 there for several months. Now your loss totals more than

$2000. You make a note to call your agent the following day and ask: will

my insurance cover this?

3. You

can't believe it! Although your inventory records say you have 50,000

widgets in stock, there are only 1000 in the warehouse. What happened

to the other widgets? Lost? Stolen? Never delivered? As your heart

sinks over the lost sale, you think: will my insurance cover

this?

4. You

watch sullenly, held motionless by the gun, as the thief cleans out

the cash from your register. As fear mixes with anger, its doubtful

that you're presently asking yourself: will my insurance cover

this?

The

quick answers to the above are partially, possibly, unlikely and

maybe.

One of

the often confusing attributes of crime insurance is that the terms

used in the insurance policies reflect legal definitions, not the

meanings we assume in everyday conversation. For example, in relating

any of the above situations to a friend, you may describe all four as

"I was robbed" or "that thief took everything I had!"

Yet,

according to an insurance policy, the above incidents are four very

different types of claims, and are described by four different, and

sometimes mutually exclusive, terms. In order of their appearance,

the terms are burglary, employee dishonesty, disappearance

and robbery. All of them, once connected to a dishonest act,

are considered a form of theft.

The

significance of knowing these terms, and the types of crime each

refers, is that you purchase crime insurance to cover each crime or

combination. For example, if your crime policy only provides burglary

coverage, only the first scenario above would be a covered loss. If

your policy only covers robbery, then only the last of the

four would be covered.

So, if

you want to be sure you have the proper crime insurance, do you have

to memorize a batch of legal definitions, or risk buying the wrong coverage

for your business? No, you just need a good agent or agency (like

us!) who deal with crime insurance and already familiar with the

vagaries, and can make sure you get the coverage most needed by your

business.

There

are a couple basic issues to consider with crime insurance. First

off, what is it you are afraid will be the focus of the crime? For

some businesses, cash is their biggest exposure. For other

businesses, merchandise may be the key target. A jewelry store may

have little cash on hand and a guard on duty during store hours.

Their real exposure may be the risk of someone breaking into the

store safe and making off with a small fortune in merchandise.

Second,

who is most likely to commit the crime? For many businesses, the real

exposure isn't someone outside the business trying to break in, but

rather someone inside the business carrying the property out. It will

do you no good to put bars on the windows, install a state of the art

security system and then hand the keys to an employee you hired last

week and say, "be sure to lock up on your way home." Do you

have a bookkeeper, cashier or store clerk who can readily walk out

the door with your property?

For other businesses, particularly those with few or

no employees, the greatest exposure will clearly come from the

outside. Below is some sample policy language from some of the

more common policies we sell concerning various forms of theft.

The exhibits linked to above are used as examples

only. Always read your policy, as the language in it may

differ. A criminal may steal your stuff. Don't let poor

insurance planning and protection steal your dream.

Portions

of this article were culled from the Trusted Choice website.

Illinois Gaming Update

Earlier this summer the Illinois Gaming Board began

taking applications online for gaming licenses. Prior copies of

applications have circulated around these last few years as Illinois

moved closer to adopting legalized video game gambling. Last

August, we passed along some tips to

help you prepare for the very thorough document and background check

the Illinois Gaming Board has.

But now the machines are going live. The app can

be found at https://www.igb.illinois.gov/vla/.

Here are some things to keep in mind as you prepare to file your

application:

Having

the first application in does not mean first application

approval. The IGB conducts an exhaustive review of

applicants and that process may take longer with some applicants

than others.

Make

absolutely sure that information is accurate and truthful.

You

cannot submit your application, withdraw it, and resubmit

it. It has to be right the first time.

It's

recommended that applicants have another set of eyes look over

their application before submitting to verify the completeness

of the app.

We know this

is a law many of you have been watching closely and anxiously awaiting

the passage of. We'll pass along any further information on

this subject as it comes out. If your business has your

machines in, we'd love to hear feedback about them, the process of

getting approved and getting your machines in, and the results you're

seeing so far. Has it been worth it? More trouble than

it's been worth? Start a discussion on our Facebook page.

Personal Articles - Are

Yours Covered?

If you

believe Hollywood's depiction of a typical heist, you'd think that

only cars and cash are the targets for thieves looking to strike it

rich. Not so. There are tons of cases involving stolen antiques, art,

and collectibles. While reading an article about a March 2012 case

where a thief conspired and stole historical documents from museums

in Pennsylvania, New York and Connecticut, then sold them for profit,

we came across an FBI statistic that estimated $4.6 billion in in

lost property in 2010.

A good

portion of that was stolen collectibles. Of all burglaries recorded,

nearly 74 percent were burglaries of residential properties. Top

targets for burglars entering a home include: electronics, jewelry,

art, antiques, collectibles, and rare items.

It's an

insurance agent's job to help clients protect what they collect.

Typical homeowners' coverage may fall short to protect the valued

collections of personal lines customers: at the time of claim,

sublimits for collections may restrict coverage well below the value

of a collection. A homeowners policy likely does not cover risks such

as accidental breakage, flood and earthquake.

First,

let's look at some of the more sought-after collectibles and the

risks they present.

Antiques

Antique

collections are the most targeted item for thieves because they're

hard to trace and easy to resell. There seems to be a recent

fascination with antiques in the last decade or so, with shows like

PBS' Antiques Roadshow and the History channel's Pawn Stars

and American Pickers sending folks digging through their

parents' basement and/or buying up vacated storage units hoping

to find treasure among trash. Some thieves even go to extreme measures to get their target.

Sports

Cards

Similarly

targeted, but only very rare cards collected by active collectors

would be difficult to unload without attracting attention.

Coin

Collections

One of

the more sought after items for thieves, coins are easy to steal and

seemingly easy to dispose of. Even so, some thieves seem to have no

idea how valuable some of the coins can be. A collector in Oregon was reunited

with most of his collection after thieves deposited them in a

supermarket coin counting machine. They got $450, but the collection

was worth several thousand dollars.

An

upward trend in gold and silver prices is boosting the appeal of

stealing coin collections. Here's one example of an uninsured loss of over $160,000.

Fathers,

lock up your daughters - or rather, your daughters toys. Barbie dolls

are sought-after collectibles. One collection of 25 dolls valued at $2000 was stolen

in Virginia in the last year. The motherlode of all Barbie stashes

though - 5000 dolls - was valued north of $1 million at the time of

it's theft in 1992. That loss was also

uninsured, although the collection was recovered later that same year.

Entertainment,

Media, Movie and Record Collections

When a

California man pleaded guilty in March to stealing

movie posters and reselling them, the victim (CBS) valued the posters

at $450,000.

Figurines

Your

great-aunt's figurines aren't just pretty - they may also be

valuable. A St. Louis woman was sentenced to a year in jail for stealing Steuben Crystal glass figurines valued

at $15,000 from a local residence.

Firearms

and Fishing Gear

Guns

are a popular target for thieves. In one instance, a firearm dealer returning home from a

gun show had more than $200,000 in guns stolen from his truck as he

sat inside a restaurant.

Military

Gear and Historic Collections

Any

item of historic significance can be stolen and may be valuable. Take

the case of the Civil War flag from the Indiana War Memorial

Museum that was swiped in 1997. It took 10 years, but the

flag was finally returned when an antiques dealer spotted the flag

while visiting a business liquidation sale and notified the FBI. The

flag, valued at $50,000, is now back with the museum.

There are collectors and valuable

collections on every American street. All it takes is the right

thief to recognize the value of certain collectibles. There's

a litany of uninsured horror stories we could link to, so

how do you properly protect your stuff?

How to Insure Your

Valuables

Some of your special possessions

covered under your homeowners policy may be severely underinsured, or

even completely uninsured. Homeowners policies may cover

certain items such as jewelry, electronics and other valuables.

However, the amount of coverage is often limited. Depending on the

item, the coverage may be anywhere from $500 to $2500 and may include

a deductible.

For example, your jewelry

may be included on your Homeowners policy under Coverage C - Personal

Property for any type of loss covered under the

policy. Unless your jewelry is stolen, in which case you may

have a sublimit of just a couple thousand dollars.

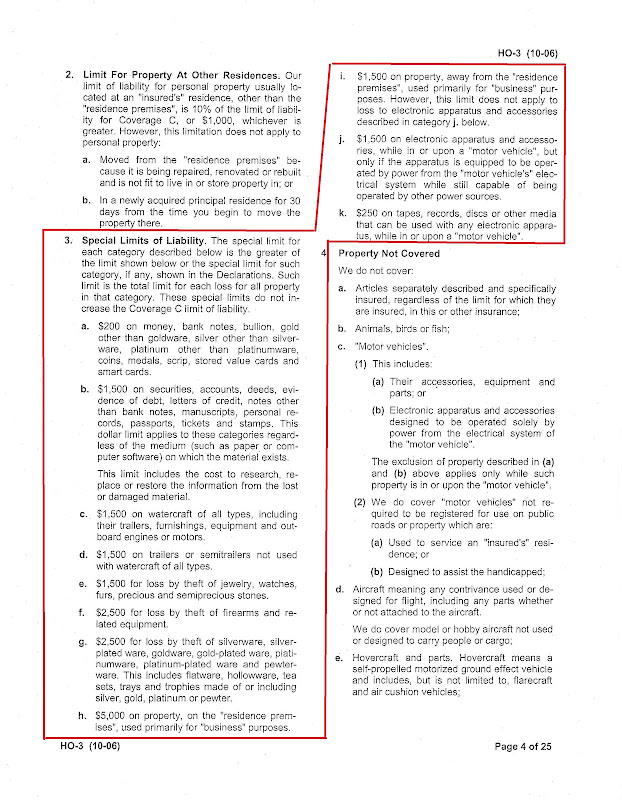

Special

Limits on Personal Property, from a sample Travelers Homeowners

policy. Click here to enlarge.

How can you insure your valuables

that may not be covered, or covered adequately, by the Personal

Property section of Homeowners policy? The solution would be to add a

personal articles floater (PAF, for short) to your policies. Depending

on the carrier, a personal articles floater may be a separate policy

or a supplemental rider added to your Homeowners policy.

What can be covered

under a personal articles floater?

If you own any of the following,

you may want to ask about whether they are protected under your

current homeowners insurance policy or if you need a PAF:

Jewelry

Artwork,

including paintings, statues, rugs, etc...

Furs

Cameras

& video equipment

Musical

instruments

Sporting

equipment

Stamps

& coin collections

China,

crystal & silverware

Why use a Personal

Articles Floater?

An item's value is not the only

consideration when determining whether to buy a PAF policy. The

type of peril to protect against should be considered, whether a

stone falls out of your engagement or wedding ring or you computer is

damaged in a flooded basement. These are damages typically

covered under a personal articles floater policy versus a homeowners

policy.

Depending on where you buy your

policy, you can either itemize your valuable items on a separate

personal articles floater or list your items on a blanket

coverage. Insurance companies have different requirements

depending on the item(s) and respective value(s).

If you have appraisals for your

valuables, you should be able to get the PAF written on an

"Agreed Value" basis. Having an appraisal on a piece

of artwork means that if you were to file a claim, you would be

reimbursed for the appraised value.

If you don't have appraisals but

have some sort of proof of purchase, such as a receipt, the total of

all items would be included on a blanket coverage. However, the

coverage is based on replacement cost or actual cash value versus agreed

value. So you may not be covered for the full amount of what you

paid for the actual lost piece.

Regarding "pair and

set" coverage, which would be used for jewelry including

earrings or an engagement ring and matching wedding band, the carrier

will reimburse you for the full cost of the pair or set as long as

you surrender the existing pieces you have in your possession to the

carrier. In other words, if the policy reimburses you for the

loss of one earring and you have to buy a pair to replace them, you

have to surrender the other earring as part of the claim.

How to Buy a Personal

Articles Floater

Here are some steps to make sure

you're buying the proper policy for insuring your jewelry and other

valuables:

List

your valuables. If you have a

collection of items you would like to insure, provide a list of

these items to your agent. The list should include a

detailed description of each item and their appraised or

purchased value. An appraisal is typically acceptable if

it was done within the last 5 years.

Check

your policy provisions for newly acquired property. What

happens if you buy a new piece of artwork or jewelry after the

policy is in place? Make sure you understand what you have

to do to get it covered under the policy.

Is

there a deductible? Ask your agent if the

personal articles floater has a deductible and if you can adjust

the size of the deductible to minimize the premium cost.

Keep

photos or video of your valuable items in addition to appraisals

and proof of purchase.

You'll need these in case you ever have to file a claim, so be

sure to keep them in a safe deposit box or scan them and keep

several electronic copies in different locations.

Consider

installing an alarm system in your home.

Increased home security should translate into a discount on your

premium.

Can

you store your jewelry and other valuables off-site?

If the items can be placed in a bank safety deposit box, this

will also qualify for a significant savings on the policy

premium.

We've written in the past about Mine Subsidence (Spring 2007, Spring 2010, Summer 2011) - usually in the

spring, when the ground softens and thaws, as that's generally when

there are more incidents of Mine Subsidence.

But there was one recent incident of Mine Subsidence

that caught our attention. The US Ice Sports Complex in

Fairview Heights, Illinois recently sank due to mine subsidence.

We've heard some parts have dropped as much as 22 inches. The

ice surfaces are cracked, the building has structural damage and all

events at the facility have been shut down since October 8th until

further notice.

In one interview we caught, a representative from the

Illinois Department of Natural Resources (IDNS) said the mine

the rinks sit atop of was closed in 1954 and runs 150 feet

deep. Much of the Metro-East area has a history of

mining. The Illinois State Geological Survey Prairie

Research Institute out of the University of Illinois has an interactive map tool, where you can

enter your address and see known mines in your area.

We've tried to find similar tools for Missouri and

Indiana. This link seems to be the best we

could dig up for Missouri, although the mapping tool seems slow and a

bit clumsy to use. Indiana has a decent mapping tool,

where you can also search by address.

Now, the problem with mapping tools is

two-fold. First off, older mines may never have been

mapped, period. Secondly, they may have been recorded

before the days of GPS, which may lead to some margin for error with

the maps. Heck, the Indiana Geological Survey out of the

University of Indiana has a plea for citizens on their homepage, urging

them to turn any old mine maps they find over to them, so that they

may update their own mapping tools.

It's unknown whether or not the US Ice Sports Complex

had mine subsidence insurance, but we would venture to guess they

did, given that Fairview Heights, IL is known to be greatly

undermined. But there could be another problem. In

Illinois, the maximum amount of mine subsidence on a commercial

property through the Illinois Mine Subsidence Insurance Fund is

$750,000. The extent of the damage is unknown, but it would not

be a stretch to imagine damages running past that amount. Mine

Subsidence coverage is available beyond that amount, but not through

the fund. Additional coverage would've needed to be purchased

through another insurance market, which can be difficult to find and

expensive to obtain.

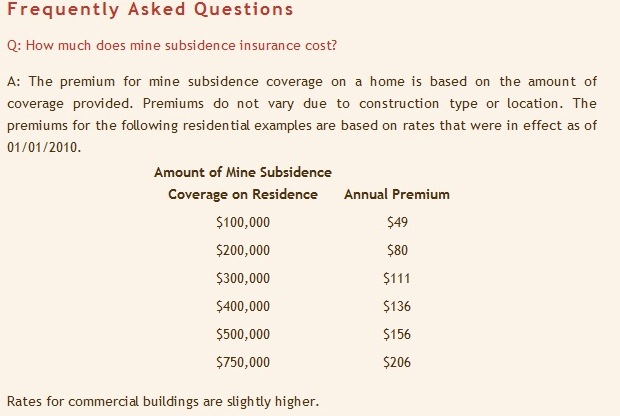

Residential

Pricing for Mine Subsidence coverage in Illinois.

The maximum available on homeowners policies is

$750,000 through the fund. Mine Subsidence coverage is fairly

inexpensive, as depicted above.

Missouri does not have a state-run Mine

Subsidence insurance fund, only a fund to repair land, not

property. Structural repair is the responsibility of homeowners

and their insurers, if their insurers offer the coverage themselves.

Indiana, like Illinois, also has a state-run Mine

Subsidence Program. The maximum limit available is $200,000 per

structure. Here are some additional details about Mine Subsidence

coverage in Indiana. Again, to get Mine Subsidence

coverage in excess of the maximum amount under the state fund, you

would have to find coverage through another insurer issued on a

separate policy, which can sometimes be tricky to find and expensive

to purchase.

According to the Department of Transportation, traffic accidents happen

about that many times an hour across the United States. Are your

personal auto limits up to par? Or are you carrying low-limit,

cut-rate coverage?

We

offer a full-line of personal lines coverages for home, auto, boats,

motorcycles, RVs and more. Give us a shot at your next renewal to

see how we compete.

Carrier Corner

We represent over 15

insurance carriers directly and have access to many more via brokers,

but you may only know one or two that we deal with. Each issue,

we'll highlight one of our valued partners in this space.

Stonegate

Insurance

Stonegate

is a newer insurance company that we have just contracted with in the

last 2-3 months. Right now, they only operate in Illinois

and are not yet rated by A.M. Best or any other 3rd party analysis

firm.

Stonegate's

appetite is what led to us giving them a shot. In addition to the

usual Personal Lines risks - home, auto, condos, renters,

and rental property, their goals for desired Commercial

Lines accounts closely aligns to what we write the most of -

hospitality businesses of all shapes, sizes and characteristics, used

auto dealers and small-to-medium contractors.

We

know they won't be a fit for everyone. Whenever possible, we'd

much rather place your insurance with a company that's highly rated and

more experienced. But they may be an alternative for some of our

clients with fewer options.

Our office will observe the following holiday schedule.

Wednesday, 11/21

Noon close

Thursday, 11/22

office closed

Friday, 11/23

office closed

Tuesday, 12/25

office closed

Tuesday, 1/1/2013

office closed

We wish you and your family a safe and happy

holiday season, and best of luck in 2013.

Bret Dixon Insurance recently became a Trusted Choice

Agency. Learn more about ithere.